Credit Limit vs Cash Limit: Key Differences, Charges & Credit Score Impact

Confused about credit limit vs cash limit? Here’s how to tell them apart and how each impacts your credit score.

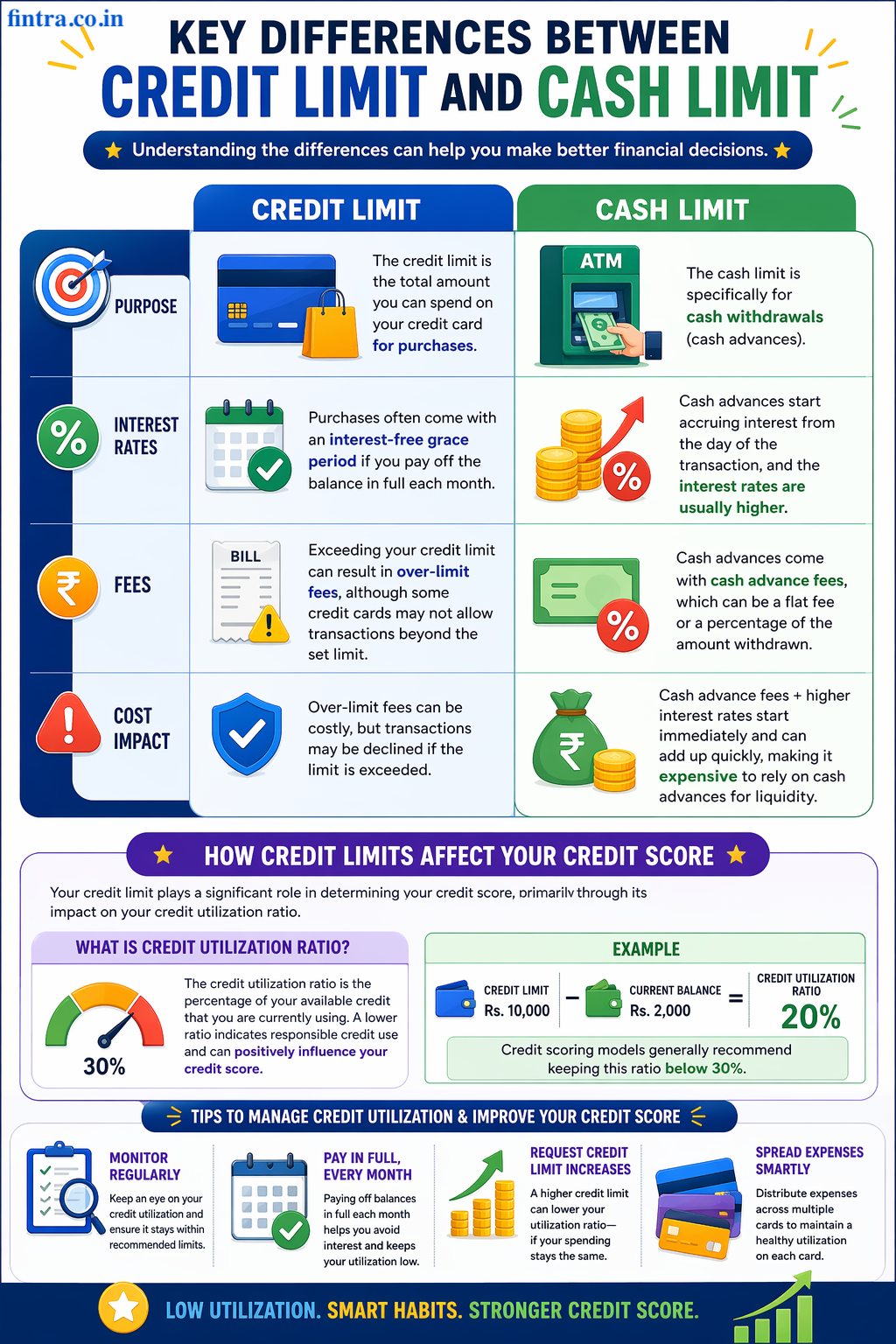

Your credit card lists two amounts: credit limit and cash limit. They’re different, and mixing them up can cost you.

In this guide, we’ll break down:

- What do credit limit and cash limit mean

- Key differences between them

- Charges and interest involved

- Their impact on your credit score

- Smart tips to manage both

Confused about credit limit vs cash limit on your credit card? Understanding the difference is crucial—especially in India, where cash advance charges and interest rates can be extremely high. In this guide, we break down credit limit vs cash limit, fees, interest, and how each affects your credit score.

What is a Credit Limit?

A credit limit is the maximum amount you can spend on your credit card for purchases, as approved by your bank based on your income, credit score, and repayment history.

A credit limit refers to the maximum amount of credit that a financial institution extends to a borrower through a credit card. This limit is determined based on various factors such as your credit score, income, and repayment history. Essentially, it's the ceiling on how much you can spend using your credit card without incurring penalties or fees.

When you receive a credit card, the issuing bank will inform you of your credit limit. This limit dictates your purchasing power and is a crucial aspect of your overall credit profile. For instance, if your credit limit is Rs. 5,000, you can make purchases up to that amount. Exceeding this limit will result in over-limit fees and may negatively impact your credit score.

It’s essential to understand that the credit limit is not a recommendation to spend up to that amount. Instead, it’s a boundary set by the bank to manage risk and ensure responsible borrowing. Maintaining a balance well below your credit limit can positively affect your credit score and demonstrate financial prudence.

|

Feature |

Credit Limit |

Cash Limit |

|

Usage |

Purchases |

Cash withdrawal |

|

Interest |

After grace period |

Immediate |

|

Fees |

Low |

High |

|

Limit Size |

Full limit |

20–40% of credit limit |

What is a Cash Limit?

A cash limit (also called cash advance limit) is the maximum amount you can withdraw as cash using your credit card from an ATM. In India, this is usually 20%–40% of your total credit limit and comes with high interest rates and cash withdrawal fees.

The cash limit on your credit card is the maximum amount you can withdraw as cash from an ATM or a bank. This limit is usually a fraction of your overall credit limit and is determined by the issuing bank based on several factors, including your credit score, income level, repayment history, and the specific type of credit card you have. Some premium cards may offer higher cash limits, while basic cards may have more restrictive terms. In some cases, you can request a review or increase of your cash limit by contacting your bank, although approval will depend on your financial profile and the bank’s policies. The cash limit is designed to provide liquidity in emergencies but comes with higher interest rates and fees compared to regular card purchases.

For example, if your credit card has a total credit limit of Rs. 5,000, your cash limit might be Rs. 1,000. This means you can withdraw up to Rs. 1,000 in cash, but doing so will typically incur higher interest rates, often starting from the day of the withdrawal. Additionally, there may be cash advance fees, which can be a percentage of the amount withdrawn.

It's crucial to use the cash limit sparingly due to the high costs associated with cash advances. Unlike regular credit card purchases, where you might have an interest-free grace period, cash advances begin accruing interest immediately. This can quickly lead to significant debt if not managed properly. Instead of relying on cash advances, consider safer and more cost-effective alternatives such as using your debit card, tapping into emergency savings, or exploring personal loans, which often come with lower interest rates and fees. These options can help you handle financial emergencies without the added expense and risk of a credit card cash advance.

Key Differences Between Credit Limit and Cash Limit

The primary difference between a credit limit and a cash limit lies in their purpose and associated costs. The credit limit represents the total amount you can spend on your credit card for purchases, while the cash limit is specifically for cash withdrawals. Understanding these differences can help you make better financial decisions. In India, credit card cash withdrawals typically attract 2.5%–3% fees and interest rates of 30%–45% annually, making them one of the most expensive borrowing options.

Interest rates are another critical difference. Purchases made within your credit limit often come with an interest-free grace period if you pay off the balance in full each month. In contrast, cash advances start accruing interest from the day of the transaction, and the interest rates are usually higher. This makes cash withdrawals a more expensive option.

Fees also differ significantly between the two limits. Exceeding your credit limit can result in over-limit fees, although some credit cards may not allow transactions beyond the set limit. On the other hand, cash advances come with cash advance fees, which can be a flat fee or a percentage of the amount withdrawn. These fees can add up quickly, making it costly to rely on cash advances for liquidity.

How Credit Limits Affect Your Credit Score

Your credit limit plays a significant role in determining your credit score, primarily through its impact on your credit utilization ratio. The credit utilization ratio is the percentage of your available credit that you are currently using. A lower ratio indicates responsible credit use and can positively influence your credit score. For instance, if you have a credit limit of Rs. 10,000 and your current balance is Rs. 2,000, your credit utilization ratio is 20%. Credit scoring models generally recommend keeping this ratio below 30%. High utilization can signal to lenders that you are over-reliant on credit, which can negatively affect your credit score.

Regularly monitoring your credit utilization and ensuring it stays within recommended limits is crucial for maintaining a healthy credit score. Paying off balances in full each month, requesting credit limit increases, and spreading expenses across multiple cards are effective strategies for managing credit utilization and improving your credit score.

The Impact of Cash Limits on Withdrawals and Transactions

Cash limits directly affect your ability to withdraw cash using your credit card. While having access to cash can be convenient in emergencies, frequent use of cash advances can lead to financial strain due to high interest rates and fees. Understanding the implications of cash limits can help you use this feature wisely.

Exceeding your cash limit is generally not possible, as most credit cards will decline transactions beyond the set limit. This can be a safeguard against accumulating excessive debt. However, it's essential to be aware of your cash limit to avoid situations where you might need more cash than your limit allows.

Using cash advances frequently can also impact your credit score, albeit indirectly. High cash advance balances can increase your overall credit utilization, which, as mentioned earlier, can negatively affect your credit score. Additionally, the high costs associated with cash advances can lead to larger outstanding balances, further straining your finances.

Managing Your Credit and Cash Limits Effectively

Effective management of your credit and cash limits is crucial for maintaining financial stability and a good credit score. One of the most effective ways to manage your credit limit is to keep track of your spending and ensure it stays well below the limit. Regularly reviewing your credit card statements can help you monitor your spending habits and make necessary adjustments. Another important aspect of managing your credit and cash limits is timely bill payments.

Late payments can result in fees and negatively impact your credit score. Setting up automatic payments or reminders can help you stay on top of your due dates and avoid missing payments. When it comes to cash limits, it's best to use cash advances sparingly. Consider alternative options for obtaining cash, such as using your savings or seeking a personal loan with lower interest rates. If you must use a cash advance, aim to repay it as quickly as possible to minimize interest charges and fees.

Tips for Increasing Your Credit Limit

Increasing your credit limit can provide more financial flexibility and positively impact your credit score by improving your credit utilization ratio. One way to increase your credit limit is by demonstrating responsible credit behavior. This includes making timely payments, keeping your credit utilization low, and maintaining a good credit score. You can also request a credit limit increase directly from your credit card issuer. When making this request, be prepared to provide information about your income, employment status, and financial obligations. Highlighting any positive changes in your financial situation can improve your chances of approval.

Another strategy is to open a new credit card account. While this will increase your overall available credit, it's important to manage the new account responsibly to avoid accumulating debt. Additionally, opening a new account may result in a temporary dip in your credit score due to the hard inquiry, but responsible use can lead to long-term benefits.

Common Myths About Credit and Cash Limits

There are several myths surrounding credit and cash limits that can lead to misconceptions and poor financial decisions. One common myth is that carrying a balance on your credit card improves your credit score. In reality, paying off your balance in full each month is more beneficial for your credit score and helps you avoid interest charges. Another myth is that requesting a credit limit increase will always harm your credit score. While a hard inquiry may temporarily lower your score, the long-term benefits of a higher credit limit, such as improved credit utilization, often outweigh the temporary impact.

Many people also believe that using cash advances is equivalent to making purchases with a credit card. As discussed earlier, cash advances come with higher interest rates and fees, making them a more expensive option. Understanding the true costs associated with cash advances can help you make more informed financial decisions.

Conclusion

Understanding credit limit vs cash limit helps you avoid high-interest debt and make smarter financial decisions. While your credit limit is designed for everyday spending, your cash limit should only be used in emergencies due to high charges and immediate interest. In short, by comprehending how these limits work and their impact on your credit score and overall financial health, you can make more informed decisions and avoid common pitfalls.

Managing your credit limit involves keeping your spending in check, making timely payments, and regularly monitoring your credit utilization. These practices can help you maintain a good credit score and ensure financial stability. On the other hand, using your cash limit sparingly and repaying cash advances promptly can prevent high-interest debt and additional fees. Ultimately, being knowledgeable about your credit card limits and how to manage them effectively can lead to better financial health and greater borrowing power. By making informed decisions and practicing responsible credit behavior, you can navigate the complexities of credit with confidence and achieve your financial goals.

Frequently Asked Questions (FAQs)

- Can I withdraw my full credit limit as cash?

No, you can only withdraw up to your cash limit, which is a portion of your total credit limit.

- Does a cash limit affect credit score?

Not directly, but high cash usage can increase your credit utilization and negatively impact your score.

- What happens if I exceed my credit limit?

Your transaction may be declined, or you may be charged an over-limit fee.

- Is cash advance bad for credit?

It’s not “bad” directly, but it is expensive and can lead to higher debt, which can hurt your score.

- Do cash withdrawals have an interest-free period?

No. Interest starts immediately from the day of withdrawal.

- How can I increase my credit limit?

You can request your bank, maintain a good credit history, and show higher income stability.

- How is my cash limit specifically determined by my bank, and can I request an increase?

In India, it is usually a fixed percentage of the total credit limit, typically ranging between 20% to 40%. However, the exact amount is determined by your bank based on several risk and eligibility factors.

Key factors banks consider:

- Total credit limit approved on your card

- Credit score (CIBIL score) and repayment history

- Monthly income and employment stability

- Existing loans and EMI obligations

- Credit utilization ratio (how much of your limit you use)

- Past credit card behavior, including late payments or defaults

As per standard banking practices regulated by the Reserve Bank of India, banks restrict cash limits because cash withdrawals carry a higher risk compared to regular purchases.

You usually cannot directly request only a cash limit increase. However, you can:

- Request a credit limit increase, which may automatically raise your cash limit

- Update your income details with the bank

- Maintain a strong repayment record

Over time, banks may revise your cash limit automatically based on your improved credit profile.

- What are safer or cheaper alternatives to using a cash advance in emergencies?

It’s smart to consider alternatives that come with lower interest rates and fewer charges.

Better alternatives to cash advance:

A. Use your savings or emergency fund

- No interest or fees

- Best option for short-term needs

B. Personal loan from bank or NBFC

- Lower interest rates than credit card cash withdrawals

- Structured repayment through EMIs

C. Credit card EMI conversion

- Convert large purchases into EMIs

- Lower interest compared to cash advance

D. Borrow from family or friends

- Usually interest-free

- Flexible repayment

E. Overdraft facility (if available)

- Linked to your salary or savings account

- Lower cost than credit card interest

Compared to these, cash advances often carry:

- Interest rates of 30%–45% annually

- Immediate interest (no grace period)

- Additional transaction fees

- How quickly does a cash advance affect my credit score or report if not repaid promptly?

A cash advance does not instantly reduce your credit score, but its impact can show up very quickly—within one billing cycle if not managed properly.

Here’s how it affects your credit score in India:

- Immediate impact on credit utilization

- Cash withdrawal increases your outstanding balance

- This raises your credit utilization ratio

- High utilization (above 30–40%) can lower your score

- No interest-free period

- Interest starts from day one

- The outstanding amount grows quickly

- Impact after billing cycle

- If not repaid by the due date:

A. Reported to credit bureaus like CIBIL

B. Late payment fees + penalties applied

4. Long-term impact

- Repeated high balances or missed payments

- Can significantly reduce your credit score

In short:

- Within days: utilization impact

- Within 30–45 days: payment history impact (if unpaid)

- Are there any hidden fees or conditions for cash advances that I should watch out for?

Yes — cash advances in India often come with multiple charges that are not always obvious upfront.

Common hidden fees and conditions:

A. Cash advance fee

- Typically, 2.5% to 3% of the withdrawn amount

- Minimum charge (Rs. 300–Rs. 500)

B. No interest-free period

- Interest starts immediately from the withdrawal date

C. High interest rates

- Usually 30%–45% per annum

- Much higher than purchase transactions

D. ATM charges

- Additional fees for using non-bank ATMs

E. GST on charges

- GST applicable on interest and fees

F. Daily interest compounding

- Interest compounds daily, increasing the total repayment

G. Limit restrictions

- You cannot exceed your cash limit, even if credit limit is available

H. Impact on rewards